Background

Sometimes it’s important to take a longer view to understand what’s happening in an industry. So, while we’ll report out on the fourth quarter on the Index call on Jan. 18, we thought it would be a good idea to start the year off with some perspective on what has happened with demand over the past few years and how that may impact 2024.

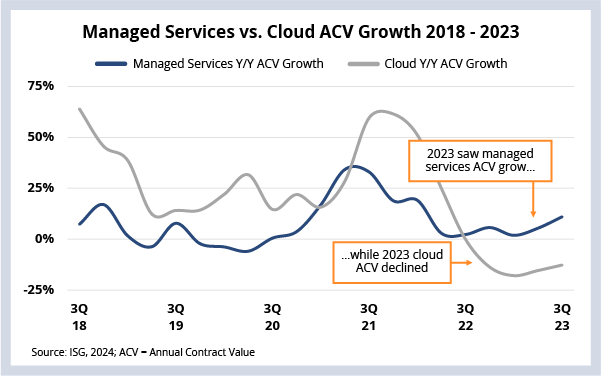

As you can see in this week’s Data Watch, managed services ACV grew by over 6% through the third quarter of 2023 – almost double its historic growth rate. Over the same time, cloud ACV declined by 16%. This happened because companies are using outsourcing to optimize costs, while they buckle down on discretionary spending, which has had an outsized impact on cloud bookings.

But if you look over a longer term, you can see that the two markets tend to move in sync. And that’s because enterprises buy and use services from both sectors. And each sector is dependent on the other for growth.

So what does all this mean for 2024? Four out of the ten

predictions we published before the holidays were related to demand, so here’s a recap:

2024 Demand Predictions