What's Next

There’s another big change over the past 10 years.

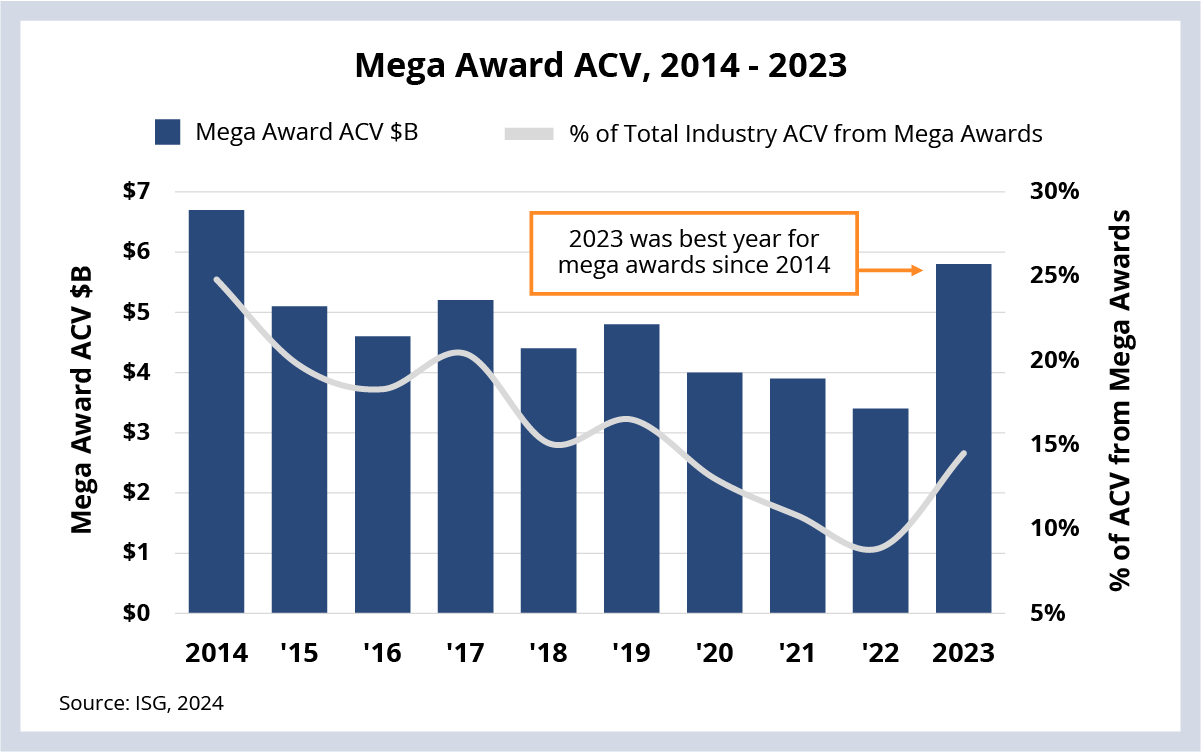

A decade ago, mega deals were infrastructure-heavy. Lots of IT assets got moved to a provider, and the provider managed it for less. With the advent of cloud, infrastructure outsourcing ACV started to decline, which means there were fewer assets to transfer – and this led to a decrease in mega-deal activity.

As providers recognized that these large, infrastructure-heavy deals were on the decline, they started to focus on shaping deals that combined different areas of scope, modernization, re-badging the people who supported these areas and financial engineering to create near-term value for clients.

This is not always done with an RFP. Often it’s done proactively through incumbency and relationship building. This is what we mean by

deal shaping.

Given the continued need to optimize costs in 2024 – and the fact that more providers are growing their big deal teams – we expect the environment will be conducive to more large deals in 2024.

We’ll be discussing these trends on the Q4 and full-year Index call on January 18, so make sure to

reserve your spot.