Background

The IT and business services industry has

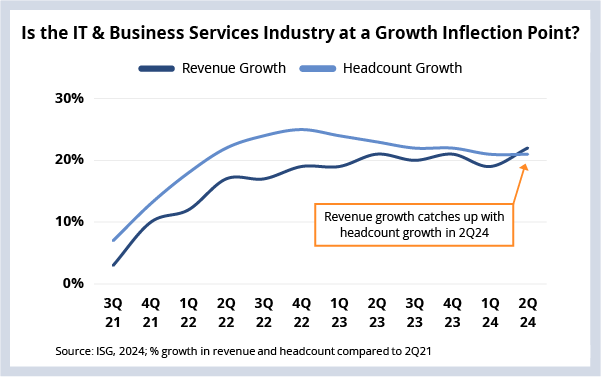

generated six consecutive quarters of annual contract value (ACV) of $10 billion or more. But, even so, growth remains sluggish as discretionary spending slows the conversion of these bookings into revenue.

As a consequence, hiring in the sector is down significantly. There have now been six consecutive quarters of headcount declines in the industry. This means the industry is smaller today by headcount than it was at the end of 2022.

But something interesting happened this quarter. As you can see in this week’s Data Watch, cumulative revenue growth for the last three years caught up – and surpassed – the corresponding change in headcount growth.

The Details